As the tide changes in real estate for the better, the affordability factor is changing as well, and for some, not so much for the better.

Buyers over the past year or so have enjoyed seeing rates below the 4% mark. And pretty stable to say the least. But with the recent fluctuation, we are almost a full percentage above where many buyers were assuming they could qualify with.

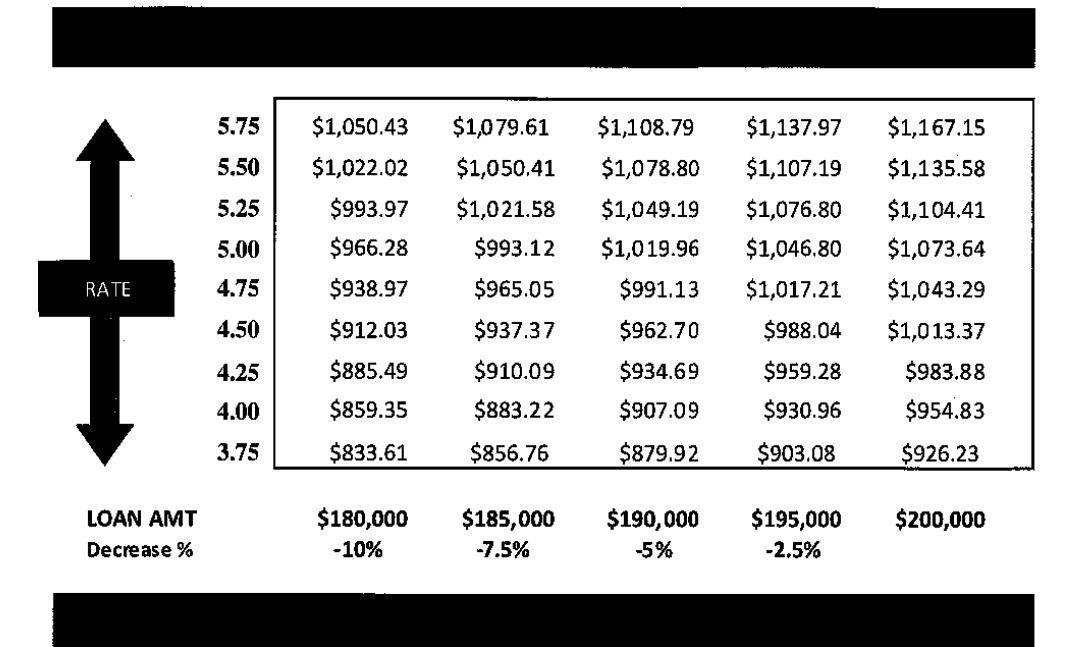

As with many buyers, the process of buying a home today is pushing their financial limits. Many buyers are facing situations where they have multiple offers to compete with when they find a home they want to buy. Usually, the bidding environment causes the offer prices to skyrocket leaving many unable to move past a small margin. We are facing situations where buyers have to go to the very limit of what they can afford. So how can a little change in interest do to these buyers? Quite a lot.

From the graph I've attached to this blog, a change of just .25% increases a monthly payment by almost $30 for a $180,000 loan. A full percentage is over $100 difference a month! So for someone looking to buy, an affordability to what they once could is no longer there. That assumption of being able to afford a $180,000 house is now really a $160,000 house. And as prices go up and interest rates follow. Buyers will be forced to rent or stay in their current homes. This can lead to a "cooling" affect on sellers and inventory will take longer to sell and prices may take a slight downhill again.

Now, don't get me wrong. This is still a great time to buy. Traditionally interest rates would be around 7-8% over historical average. So we are still well below what could be. And for buying, just like the old saying for planting a tree, if you didn't plant/buy is a few years ago, the best day to start is today.

If you are a buyer out there and shopping for a home, talk to you mortgage lender. Make sure your pre-approval is up to date and that current interest rates are taken into consideration. Then make sure you are looking at homes that fit into that budget.

As always, you can go onto my website http://rebeccatherealtor.com/ to search through the MLS and use our mortgage calculator to determine if you can afford a home, just remember to add in taxes and insurance. Good rule of thumb is $1800 per year per bill. Many times you'll be below but on some properties you can be above. Be conservative on creating your budget and you'll have more money to save and possibly invest in more real estate.

It's still the best investment you will ever make!